Yes — renters insurance does cover liability. In fact, personal liability coverage is one of the most important parts of a standard renters insurance policy, and most renters don't fully understand what it protects them against until they need it.

This post breaks down exactly what renters insurance liability covers, how much coverage you likely need, what it won't cover, and how it's different from tenant liability insurance (which is a separate thing that often gets confused with it).

Table of Contents

- What Is Renters Insurance Liability Coverage?

- What Does Renters Insurance Liability Cover?

- What Renters Insurance Liability Does NOT Cover

- Tenant Liability Insurance vs. Renters Insurance: What’s the Difference?

- How Much Renters Insurance Liability Coverage Do You Need?

- Do Utah Landlords Require Renters Insurance?

- Frequently Asked Questions

- The Bottom Line for Utah Renters

What Is Renters Insurance Liability Coverage?

Renters insurance is made up of three main components:

- Personal property coverage — protects your belongings (furniture, electronics, clothing) if they’re stolen or damaged by a covered event

- Additional living expenses (ALE) — pays for a hotel or temporary housing if your unit becomes uninhabitable

- Personal liability coverage — protects you financially if you’re found legally responsible for injuring someone or damaging their property

That third piece — personal liability coverage — is what we’re focusing on here. Most standard renters insurance policies include $100,000 of personal liability coverage by default, though many insurers let you increase this to $300,000, $400,000, or $500,000 for a small additional premium.

There’s also a fourth coverage many renters don’t know about: medical payments to others (MPTO). This is a separate, smaller coverage — typically $1,000–$5,000 — that pays a guest’s medical bills quickly and without requiring them to sue you first. Think of it as goodwill coverage: someone sprains their ankle in your apartment, you don’t want a lawsuit, so MPTO pays their urgent care bill directly. It doesn’t require you to be found negligent — it just covers reasonable medical expenses for guests injured on your property.

Renters insurance is a policy that helps protect tenants from certain financial losses by covering personal belongings, liability for accidental injury or damage to others, and in some cases additional living expenses if the rental becomes temporarily uninhabitable due to a covered event.

What Does Renters Insurance Liability Cover?

Renters insurance liability coverage kicks in when you’re held legally responsible for two main things: bodily injury to another person, or damage to someone else’s property. Here’s how that plays out in practice.

Bodily Injury to Others

If a guest slips and falls in your apartment and decides to sue you for medical bills and lost wages, your renters insurance liability coverage handles it. This includes:

- Emergency medical care costs

- Ongoing medical treatment

- Lost income the injured person claims

- Pain and suffering damages

- Your legal defense costs if you’re sued

This coverage applies whether the injury happens inside your unit or in some cases outside of it. If your dog bites a neighbor in the hallway, for example, most renters policies cover that too — though some insurers restrict coverage for certain dog breeds, so it’s worth checking your policy.

Dog bites are worth taking seriously: the average dog injury claim in the U.S. now exceeds $69,000, and total dog-related liability claims hit $1.57 billion in 2024 according to the Insurance Information Institute. If you have a dog, carrying at least $300,000 in liability coverage isn’t optional — it’s common sense. This applies to both pets and assistance animals.

Property Damage You Accidentally Cause

If you cause damage to someone else’s property — whether that’s your neighbor’s unit or the building itself — your liability coverage can help. Common examples:

- You leave the bathtub running and it overflows into the apartment below, damaging the neighbor’s floors and belongings

- You accidentally start a grease fire that causes smoke damage beyond your unit

- Your kid throws a ball through a neighbor’s window

In each of these cases, your renters insurance personal liability coverage would pay for the damage you caused to others, up to your policy limit.

Legal Defense Costs

Even if a lawsuit against you ends up being dismissed, the legal fees can be significant. Renters insurance liability coverage typically includes the cost of hiring a lawyer to defend you — this is separate from and in addition to whatever damages might be paid out.

What Renters Insurance Liability Does NOT Cover

Knowing what’s excluded is just as important as knowing what’s covered. Renters insurance personal liability coverage does not cover:

- Your own injuries. If you hurt yourself in your apartment, that goes through your health insurance, not renters insurance.

- Your own property. Liability coverage protects others — your personal belongings are covered under the separate personal property section of your policy.

- Intentional damage. If you deliberately damage someone’s property or injure someone on purpose, your insurer won’t cover it.

- Auto accidents. If you cause an accident in your car, that’s handled by your auto insurance liability, not renters insurance.

- Business activities. If you run a business out of your apartment and a client is injured, standard renters insurance typically won’t cover it. You’d need a separate business liability policy.

- Common area accidents. If a guest slips on the icy shared walkway outside your building, that’s the landlord’s liability — not yours. Your coverage applies to what happens within your unit and through your own negligence.

- Damage to the rental property itself. This is a common source of confusion — and leads us to the next section.

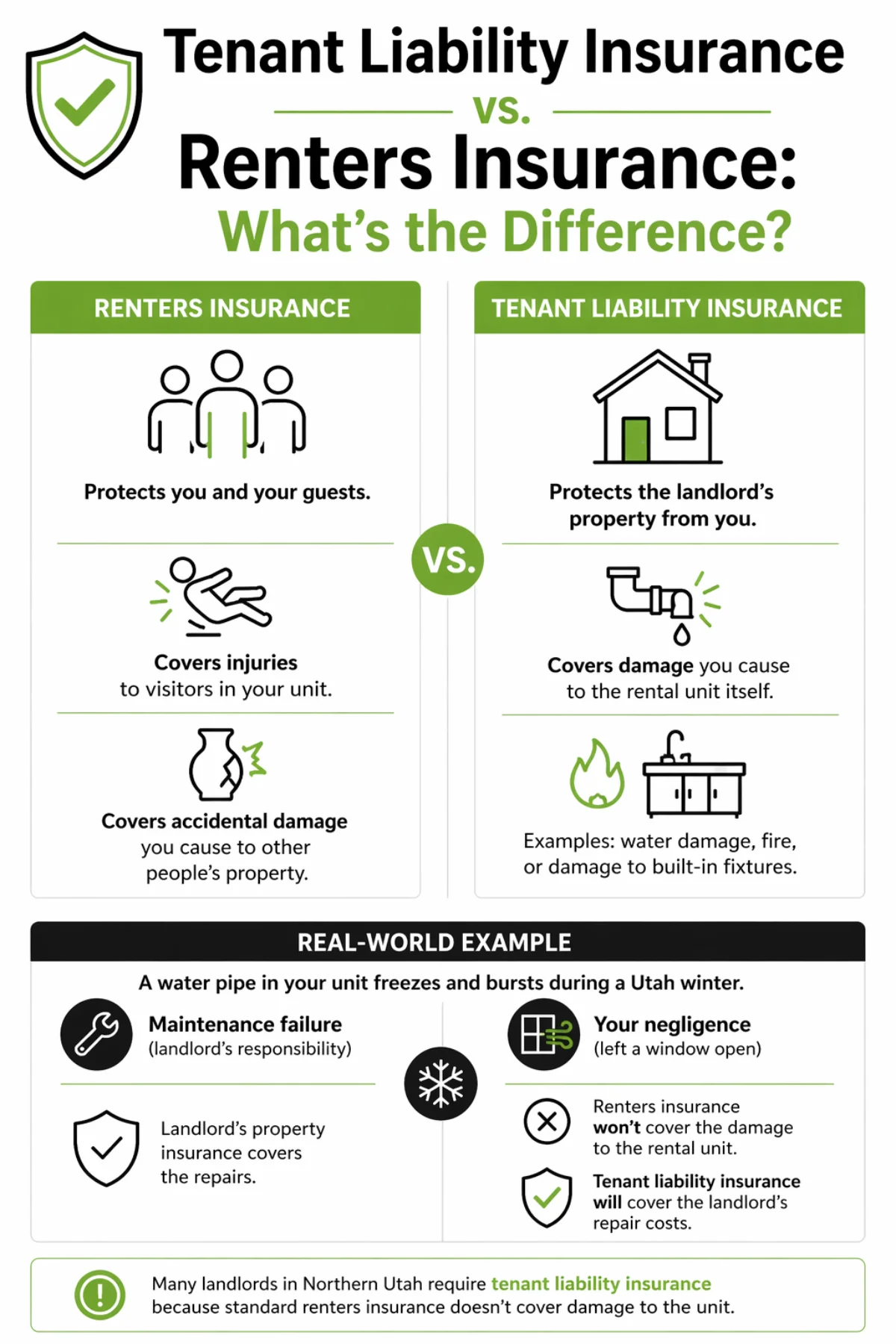

Tenant Liability Insurance vs. Renters Insurance: What’s the Difference?

This is where most renters (and some landlords) get confused, so let’s be direct about it.

Renters insurance protects you and your guests. The personal liability component covers injuries to visitors and accidental damage you cause to other people’s property.

Tenant liability insurance protects the landlord’s property from you. It’s specifically designed to cover damage you cause to the rental unit itself — things like accidentally flooding the unit, causing a fire, or damaging built-in fixtures.

Here’s a real-world example that illustrates the difference:

Say a water pipe in your unit freezes and bursts during a cold Utah winter. If the burst happened because of a maintenance failure — the landlord’s responsibility — the landlord’s own property insurance handles the repairs. But if the pipe froze because you left a window open and the temperature inside dropped, that may be considered tenant negligence. In that case:

- Renters insurance probably won’t cover the damage to the rental unit, because that’s not “someone else’s property” for liability purposes — it’s the landlord’s building

- Tenant liability insurance would cover the landlord’s repair costs, because that’s exactly what it’s designed for

Some landlords — including many in Northern Utah — now require tenants to carry tenant liability insurance (sometimes called renter’s liability insurance or a security deposit alternative) specifically because standard renters insurance doesn’t reliably cover damage to the unit itself.

Bottom line: If your lease requires “renters insurance,” read it carefully. Some landlords specifically require tenant liability insurance, which is a narrower product that covers only damage to their property. Others accept a standard renters policy with personal liability coverage. When in doubt, ask your property manager what’s required before you buy.

How Much Renters Insurance Liability Coverage Do You Need?

The standard amount that comes with most policies is $100,000. For most renters, this is enough to cover typical slip-and-fall claims or accidental damage scenarios.

However, it’s worth increasing to $300,000 if any of these apply:

- You own a dog, especially a larger breed

- You regularly host guests or gatherings

- You work from home and clients occasionally visit

- Your personal assets (savings, investments, future income) exceed $100,000

The cost to upgrade is minimal. Going from $100,000 to $300,000 in liability coverage typically adds about $12–$15 per year — not per month. That’s less than a dollar a month for double the protection.

Most insurers cap renters liability at $300,000–$500,000. If you want protection beyond that, you can add an umbrella insurance policy, which provides $1M+ in coverage across renters, auto, and other liability. Umbrella policies typically cost $150–$300 per year.

A rough rule of thumb: your liability coverage should be at least equal to your net worth. If a judgment exceeds your policy limit, the plaintiff can pursue your personal assets to cover the difference.

Do Utah Landlords Require Renters Insurance?

Utah law does not require renters to carry insurance. However, landlords are legally permitted to require it as a condition of the lease.

Many property management companies in Northern Utah — including in Salt Lake City, Ogden, Layton, and surrounding areas — now include an insurance requirement in their standard lease agreements. This is increasingly common because it reduces disputes over who’s responsible when accidental damage occurs.

If your lease requires renters insurance, make sure your policy meets the minimum coverage amounts specified. Some leases also require the landlord to be listed as an additional interested party on the policy so they’re notified if coverage lapses.

Protect Your Rental. Protect Yourself.

Have questions about renters insurance or tenant liability coverage? Our team at Envy Property Management is here to help you understand your options and stay fully protected.

Get Guidance TodayFrequently Asked Questions

Does renters insurance cover liability for a dog bite?

Most standard renters insurance policies do cover dog bite liability, meaning they may help pay for medical expenses and legal costs if you are sued. However, some insurers exclude certain breeds, so always review your policy carefully.

Does renters insurance cover accidental damage to a neighbor’s apartment?

Yes. If you accidentally cause damage to a neighbor’s unit, such as a leak that spreads, your renters insurance liability coverage may help pay for repairs up to your policy limits.

What’s the difference between tenant liability insurance and renters insurance?

Renters insurance is broader and covers your belongings, liability, and sometimes temporary housing. Tenant liability insurance is narrower and typically only covers damage you cause to the rental unit itself.

Does renters insurance cover legal fees if I’m sued?

Yes. Personal liability coverage often includes legal defense costs if you are sued for a covered incident.

How much does renters insurance cost?

Costs vary, but many policies are relatively affordable depending on your coverage limits, deductible, and location.

The Bottom Line for Utah Renters

Renters insurance does cover personal liability — and that coverage is worth far more than most renters realize until they actually need it. A single lawsuit from a slip-and-fall or an accidental flooding incident could easily exceed $50,000 in damages and legal fees. A renters policy covering that risk costs less than a streaming subscription per month.

If your landlord or property manager requires you to carry insurance, make sure you understand whether they’re asking for standard renters insurance, tenant liability insurance, or both. Those are different products that cover different things.

Not sure what coverage your lease requires? Contact your property manager directly — or if you’re a Northern Utah rental owner looking to protect your investment, reach out to Envy Property Management to talk through how we handle insurance requirements for our managed properties.

Envy Property Management is not a licensed insurance agent. This content is provided for general informational purposes only and should not be considered professional insurance advice. For guidance on specific coverage questions, please consult a licensed insurance professional.